Commodities | Feb 26 2009

By Greg Peel

What pushes the gold price? Let’s break it down.

The first, simple, equation to consider is that of demand and supply. We’ll look at demand first.

Gold is an unusual beast in that it is both a commodity and a currency. On the commodity side, there is some industrial usage of gold but the bulk of “commodity” demand is derived from the jewellery market. Indeed, so proportionately minimal is gold’s use in industry that we’ll completely ignore it within the equation. Thus we can say that gold is never consumed or destroyed. Even when a piece of jewellery or some other trinket is melted down, no gold is lost out of the sum total. This makes gold virtually unique.

I make the English grammar mistake of qualifying the word “unique” here because gold has a poorer (but still loved) cousin in the form of silver. Silver also shares a commodity/currency dichotomy but given silver is used in a wide range of industrial applications it tends to split the difference. And if you consider that even the “commodity” definition of gold jewellery is questionable, given the wife might appreciate the aesthetic but the husband sees an investment (sorry to be chauvinist here but I need to make a point), realistically it’s hard to consider gold as in any way a commodity at all. Hence while silver enjoys industrial as well as investment demand, demand for gold is almost entirely an investment consideration.

This is still the case when one considers one of the greatest sources of gold jewellery demand is middle class India. Indian tradition determines that gold is given as a gift to mark a wedding, and gold it must be – not just something else pretty. Every ancient culture appreciates the investment value of gold. Nevertheless, market observers tend to separate demand into the two categories of “jewellery” and “investment”.

Jewellery demand consumes, on average, about 75% of the world’s net gold production each year. (I say net to account for “scrap” – jewellery that has been pawned, melted down and reworked.) The other 25% is consumed by those who buy gold for its investment value alone.

Within that 25%, one might break down the source of investment demand, being simplistic here, into two types of fear – the fear of crisis and the fear of inflation.

If you have a suitcase full of cash you could invest that money into, say, a risk asset such as stocks – or put it in the bank, or put the suitcase in the cupboard. If there is a financial crisis, you will lose your money in stock. If it is a really bad financial crisis, your bank might go under with your money. In the case of crisis, perhaps the cupboard is the best bet. You’re not going to earn any interest or make a capital gain, but at least you’ll still have the money you started with.

Unless, of course, inflation is a problem. If prevailing inflation is high, the purchasing power of your cash becomes less and less. A loaf of bread that costs a dollar today could cost two dollars in ten year’s time, so after ten years you have effectively lost half your money. What you really need, then, is somewhere to safely “store” not your money, but your “wealth”. You want to at least have the same wealth value as when you started.

Enter gold. Gold pays no interest, but in times of crisis it is a popular move to get out of stocks, other risk assets, and bank deposits and get into gold because there your money will be safe. Your “wealth” will be “stored”. You can decide at a later date to move back out of gold and into stocks etc when they’re cheaper. In times of high inflation, your gold store can be converted back into cash and your one dollar from the beginning will get you two dollars today with which to buy that loaf of bread.

To confirm this supposition, consider that gold traded at its highest price in history in March last year, a time when (a) the global financial crisis was really starting to heat up and (b) emerging market demand for oil and other commodities was pushing inflation higher and higher.

Breaking down gold as an investment, one can buy gold coins, gold bullion, exchange-traded funds (ETF) and similar instruments, and gold futures. The first two mean simply buying gold, although coins also carry a numismatic value. An ETF means buying a charge over an amount of gold stored on your behalf. A futures contract means buying gold as a paper IOU.

Of the choices, a futures contract offers built in leverage. Earlier this week you could have bought a 100 ounce Comex contract for a US$4,000 deposit, whereas the equivalent in physical gold would have cost you more like US$97,000. If gold rallies then both investments will provide the same return. The only catch with futures is that if the gold price falls, you have to start topping up your deposit (a dreaded “margin call”).

There is an additional consideration in that if you buy a futures contract, your only other cost is a broker’s commission on the US$4,000. If you buy physical gold, you must either pay for it to be stored, or have it sent to you in armoured truck where you then must try and safely store it. Oh, and insure it.

(You can, of course, also “buy” gold by buying shares in goldminers, but such shares are never a simple one-for-one bet on the gold price. Goldminers have all sorts of other problems).

Note that gold futures contracts allow you to choose to have gold delivered to you at expiry, but this usually only happens to only 2% of contracts. The other 98% are closed out for cash before expiry. That effectively means the amount of gold traded each month can be levered up 50 times. And that’s on top of the leverage to cash a futures contract already provides. As gold futures can be just as easily sold short as well as bought, such leverage also exists on the supply side.

Which brings us to the supply side.

Supply includes old gold and new gold. Old gold is all the gold that ever existed, which is held as jewellery, as personal or corporate investment, or by central banks. The US Federal Reserve is the biggest holder of gold, followed by the IMF and then the legacy central banks of Europe. Sale of European central bank gold is limited to 500 tonnes per year.

New gold is that which is dug out of the ground every year, but that volume has been dwindling year-on-year for decades.

The amount of physical gold traded across the globe each year is tiny compared with that of consumable commodities such as oil. Very, very tiny in fact. Most gold is traded as Comex futures. As noted, on average only 2% of gold contracts are held for delivery. This statistic means that Comex need only hold a limited amount of physical gold in its own vault to cover potential delivery requests. Were everyone who holds a long gold contract in the middle of the trading month – when open positions are highest – to hold for delivery, there would not be enough gold in the Comex vault to satisfy the demand. There would not be enough gold in Fort Knox. There would not be enough gold in the world. There would probably not be enough gold in the world several times over.

Demand and supply of gold as an investment, therefore, is very much levered up by the “paper” gold market.

So there we have a (simple) consideration of gold’s demand/supply equation. We know that recently the gold price has again been trying to push to new highs, suggesting demand is currently winning the battle against supply. Why is this the case?

Under our simple breakdown, gold demand is coming from either the jewellery market or the investment market or both. However, I can tell you now that demand is not currently coming from the jewellery market.

One reason is that we are not currently in an Indian “wedding season” and won’t be again until about September. Jewellery demand also comes from China and the Middle East, with a similar middle class bent (rich people, wherever in the world, will always buy gold jewellery so we take them as a given). But the real reason there is little jewellery demand at present is because middle class jewellery demand is highly “price elastic”.

A commodity is “price elastic” if price makes a big difference. Bread and milk are relatively “price inelastic” because you’re going to buy them anyway even if the price ticks up. But when the price of gold ticks up, there is a point at which the jewellery buyer just has to say “too much”. Gold’s long rally from around US$250/oz a decade ago to US$1000/oz has been driven by financial market considerations, and by jewellery demand. Coming back to India specifically, we note that the Indian economy has boomed in that time. This means more money in the pockets of the middle class and that means a higher price tolerance for gold.

Every wedding season (of which there are two each year) Indians buy up gold until the price is too high. If in one year gold has rallied from US$500 to US$700 then Indian demand might dry up at US$600. What usually follows is a drift back in price for a while, until the next season. By the next season everyone is just that bit richer again, and this time will pay US$600/oz. Gold then runs to US$800/oz. Next year the Indians will pay US$700. And so has this price ratcheting effect being going on for a decade. Two steps forward and one step back.

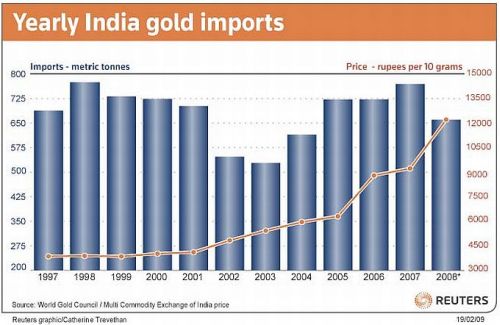

When gold hit US$1000 last year, the Indian buyers were left behind at around US$800. The last push to the summit involved a near vertical ascent. Consider the chart:

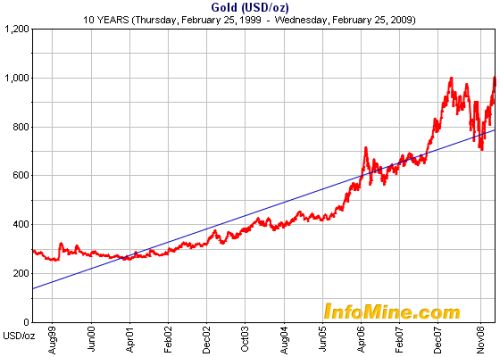

Note how jewellery demand ebbs and flows as the gold price rises. Note also that demand in 2007 was the same as that in 1998 at a much lower price. That chart has the gold price in Indian rupees, but as one can see from the next chart the exchange rate into US dollars makes little difference to the trend. India will pay more and more for its gold as long as its economy keeps growing.

And therein lies the problem – the Indian economy has slowed considerably. All economies have either slowed or receded. Even if the gold price were to fall back from US$1000 to US$800 now, we can’t be guaranteed of a return to historical jewellery demand this time. The game has changed. Jewellery demand has acted like an ever-rising safety net for the gold price in the face of financial market volatility. That safety net may well be a long, long way down this time.

But if there is no jewellery demand at present, that means investment demand is not only making up for the loss, but exceeding it. Gold has again tested its highs.

There is no surprise this might be the case, as gold investment demand is driven by fear – fear of crisis, and fear of inflation. When gold hit US$1030 last year both fears were firmly in place. The stock market was tanking, Bear Stearns was going under, and oil was on its way to US$147/bbl, pushing inflation into double digits in many countries. Jewellery demand didn’t matter.

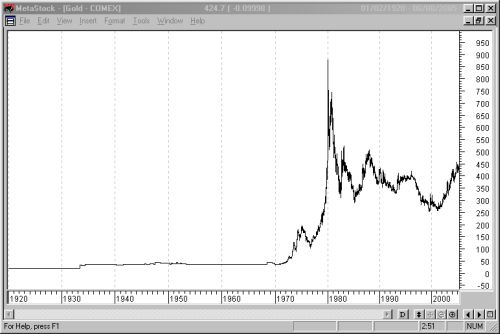

Now – with the previous USD gold graph in mind, consider this next graph of the gold price from 1920-2002:

What stands out? Is it the sudden, almighty spike in 1980? Does it not look like the ECG of someone who was just brought back from the dead?

The reason the gold price seems to flatline until 1970 is firstly due to the scale. The fluctuations up to that point don’t register much, although one can notice a decided blip in the Great Depression and a fair bit of activity around the end of World War II. But the real reason for the sudden and dramatic change in gold price was that in 1970 the US dollar became the world’s reserve currency. Prior to that point, the Gold Standard (all currencies were pegged to gold) was in place, but for a few brief departures such as wartime and the Great Depression. Beyond that point, Americans were basically free to borrow money at will.

In the 1970s, inflation exploded. Inflation had already begun rising in the sixties as the baby boomers fired up the consumer society, and everyone had to have a car, washing machine and television. But the seventies brought the oil shocks, when OPEC cut off supply. The price of oil, and everything, went through the roof. Double digit inflation caused a rush into gold, notwithstanding the general fear of a disgruntled Middle East. The peak came in 1980 when the Shah of Iran (a US ally) was deposed by the Ayatollah (anything but).

By 1980 there was simply a gold bubble, and that had to burst. Gold fell back from US$800 to US$400 rather quickly, but this was still a long way up from the US$50 of 1970. Inflation remained at high levels right through to the new boom of the eighties. The next peak was reached in 1987 when the stock market crashed.

Okay – let’s just ignore 1987-2001 for a minute and consider the period 2001 to today, for which we need to go back to the earlier chart. The gold price starts a steady rise again, but this time there is very little inflation involved. This time it is fear driving the gold price – from 9/11 to the fear that the US current account deficit is getting way too big (which in turn has sent the US dollar into a gradual decline). The surge in 2006 is a demand surge based on the introduction of gold ETFs. Suddenly everyone had ready access to the physical gold market. The surge in 2007 is the credit crisis – rather fear-inducing – and the kick in 2008 is added inflation, when oil began to surge.

Fear and inflation – the two drivers of gold.

Now let’s go back to that lost period of 1987 to 2001. Why did gold fall steadily in this period?

Economic recessions are usually demand-side driven – demand falls so prices fall, meaning low inflation. The seventies was an exception. The seventies saw a deep recession but it was supply-side driven – demand could not meet the high price of oil when supply was cut off. Hence the seventies was a rare case of recession and high inflation. High inflation lingered into the eighties boom, but when the boom turned to bust and the nineties began with recession, we were back to a typical demand-side recession again. Inflation fell, and so gold fell.

The fall in inflation in the nineties was dramatic – from double digits down to what central banks now call a “comfort zone” of 2-3%. So bad was the recession in Japan that inflation actually turned into deflation.

Consider now that across the globe, prices are falling. Inflation peaked in mid-2008 and we have experienced disinflation ever since. With the world heading into deep recession, we are now looking at deflation.

In times of deflation the price of gold tends to fall. The nineties is living proof.

But if we have been disinflating since mid last year, why is gold testing the highs? Well – because of the other fear – the fear of crisis. That fear has rarely been as great as it is now. But there is another fear as well – the fear that the US is going to print too much money to rescue its economy. The printing of money causes inflation. It can cause hyperinflation.

The quick-witted might at this point like to say: “Hang on a minute. What about the crises of the nineties? The Asian Currency crisis and the fall of hedge fund LTCM (which at the time threatened to bring down the whole financial system just like Lehman Bros did last year). Why didn’t gold rally strongly on fear these times.?

The answer to that one is that gold was heavily sold by central banks in order to support the US dollar. The UK sold half of all its gold in 1999 – gold’s low point. So much gold was sold by European banks acting in isolation that they eventually got together and set their own sales quota (the aforementioned 500 tonnes). And the world’s biggest holder of gold – the US – sold and sold and sold gold it didn’t even have.

Remember how I said that the Comex futures market allows for gold to be sold short? Well the US government has been selling gold short for decades in order to keep the reserve currency supported. It would do so by leasing gold to investment banks, who would then sell short. If the gold price still managed to rise and the banks took a loss, they would be reimbursed by the government in cash. Such an activity has now been admitted to by ex-government employees, the most recently being Paul Craig Roberts, assistant secretary of the Treasury in the Reagan administration.* Reagan took office in the early eighties. Check out the gold price.

So if you are a holder of gold, looking forward to the gold price breaking through US$1000 on its way to US$2000 (as so many people seem to suggest will happen), you will not be thrilled to consider that (a) jewellery demand has gone, (b) deflation is setting in, and (c) the US government can manipulate the gold price. If you’re still having problems with the last one, consider that when President Roosevelt abandoned the Gold Standard in 1933 in order to do something – anything – to end the Great Depression, he also confiscated the gold of all Americans. That’s why you can barely see a price hike on the graph. After World War II, the Gold Standard was reinstated.

But the above arguments are not new. Prices have been deflating since mid last year. Jewellery demand disappeared months ago. Even if the US government is selling, we are still testing the highs again. Why?

Because the US government is also printing money faster than you can blink. And that has the market very worried.

Monetarist theory suggests you can print money all you like in periods of price deflation, because the inflationary effect of printing money only cancels out the price deflation. The US Federal Reserve is of the belief the US economy will stop receding by late 2009, and President Obama has as good as vowed to print whatever money it takes to make sure that is the case. If they are right, and get it spot on, then good luck to them.

If they are wrong, and no amount of money printing avoids recession becoming depression, then the resulting lingering deflation could well send the gold price tumbling. If they are right, and fear abates, then the resulting flight back into risk assets would send the gold price tumbling. This does not sound good.

But if they are right, and the US economy recovers, what if the US government has printed way too much money? If fear abates, investors will also abandon the US dollar (they will sell US Treasuries and buy risk assets again). Gold will soar.

The market for US Treasury bonds and bills is a vital part of the equation. As long as these are being bought, the US dollar remains supported. Fear has driven investors into not only gold, but into the debt of the world’s largest economy as well. It is ironic that an economy in so much strife should be considered a safe haven, but it is all because of relativities. The economies of other nations are currently in a much worse position.

If fear abates, investors will begin to leave US Treasuries and the US dollar will no longer be supported. If the world begins to think the Americans are printing way too much money (as compared to the governments of other major economies, which are currently doing the same thing), it will abandon US Treasuries. If the US dollar collapses, gold will soar.

The aforementioned former assistant Treasury secretary had this to say:

“The Bush and Obama plans total 1.6 trillion dollars [of taxpayer money, not including printed money sterilised by bond issues], every one of which will have to be borrowed, and no one knows from where. This huge sum will compromise the value of the US dollar, its role as reserve currency, the ability of the US government to service its debt, and the price level. These staggering costs are pointless and are to no avail, as not one step has been taken that would alleviate the crisis.

“How long can the US government protect the dollar’s value by leasing its gold to bullion dealers who sell it, thereby holding down the gold price? Given the incompetence in Washington and on Wall Street, our best hope is that the rest of the world is even less competent and even in deeper trouble. In this event, the US dollar might survive as the least valueless of the world’s fiat currencies.”

And therein lies the crux. Whose economy is in the biggest trouble, and who’s going to end up printing the most? Gold’s journey from here will depend on just how long the US can reasonable hold on to the reserve currency status of the dollar, before the world yields to gold’s former role.

And much of the world is currently indicating that it prefers gold. This is not apparent in the US dollar, for the US dollar remains strong. But it is apparent in the world’s current demand for physical gold – not as jewellery – but as gold coins and bars, and ETFs.

ETF volumes have reached record volumes. Retail gold dealers began to run out of coins and bars around September last year when Lehman Bros, and the stock market, collapsed and fear peaked. Mints across the globe could not keep up with the demand. There was a brief respite, but in 2009 that demand is back stronger than ever. From the US to South Africa, from Austria to New Zealand, the demand for physical gold is soaring.

In 2007, just under 200,000 ounces of gold were sold in the US in the form of American Eagle coins. An equivalent volume was sold in the first half of 2008. An equivalent volume was sold in the first seven weeks of 2009. Across the world, dealers are selling gold in a day what they used to sell in a month. Dealers open on Monday and are sold out by Tuesday. Buyers have to wait for the next Monday to get in again, unless the Mint has run out, again.

Remember that the vast proportion of gold is traded as Comex futures. But so great is demand for physical gold at the retail level buyers are paying a 5% premium over the Comex price. And Comex futures are only an IOU. In times of financial crisis, investors prefer the real thing. The number of contracts being held for delivery has now blown out to 4.5% from 2%. In the case of silver, it’s 7.3%. These numbers are still relatively small, but remember that Comex only holds an amount of metal which would reasonably cover deliveries, not what would cover all contracts if they were all called for delivery. That much gold does not exist.

The effect of this supply-side shortage is that price-push of retail demand is not showing through into the market yet.

If jewellery demand is not with us, investment demand surely is – despite a stronger US dollar. Which way is this going to break?

*http://www.counterpunch.org/roberts02242009.html